Pensions alone currently cost the county 30 cents on top of every payroll dollar – over 65 cents if you include all benefits

By Supervisor Pat Herrity (R-Springfield)

Since elected to office in 2008, I have been working to address the County’s compensation and pension issues. Pensions alone currently cost the county 30 cents on top of every payroll dollar – over 65 cents if you include all benefits. Pension costs compete with our ability to fund the services our residents expect, compete with our ability to pay salaries that attract the best and brightest employees and teachers, and are a big reason homeowner taxes have increased 25% in the last five years.

When I joined the Board, employees could retire as early as age 50 with a pension that is significantly higher than surrounding jurisdictions. On top of that very generous pension, they also received a benefit unheard of anywhere else – a county paid social security benefit from their date of retirement until the date they are eligible to receive federal social security. I was able to get the Board to review pensions in 2013, but could only get them to raise the retirement age from 50 to 55. Thanks largely to the debate on the meals tax, the Board agreed to take another look at pension costs and began another review in late 2016.

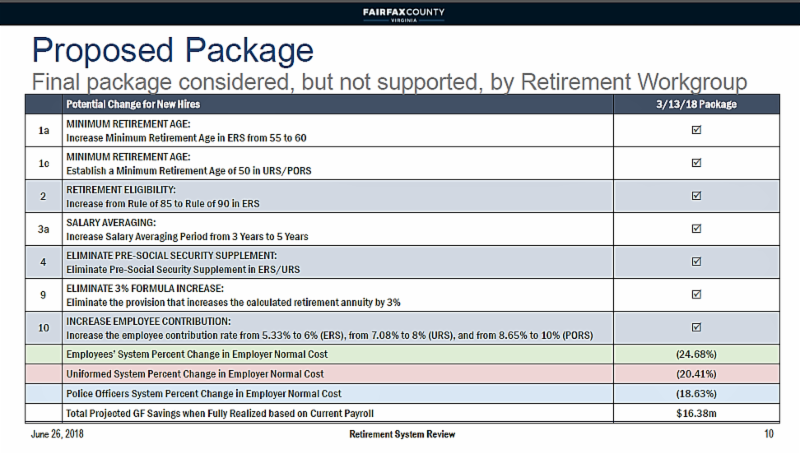

Staff proposed a number of changes to the pension plans which were presented to a working group consisting largely of employee unions. Below is a list of options presented at the Board’s Personnel Committee meeting in June, which was whittled down to just five changes:

The changes would only apply to employees hired after June 30, 2019, and if all approved, would still leave our county employees with the best pensions in the region. At the December 4th meeting, my motion to approve all five changes was only supported by Supervisors John Cook and Linda Smyth. The Board ultimately voted to approve only two of the five proposed amendments, including the elimination of the pre-social security supplement.

We still have work to do to reform our pensions. Too much of our compensation dollar still goes to pensions, our pension benefits are still much greater than surrounding jurisdictions, and the cost is unsustainable. All of Fairfax County’s pension projections are based on a 7.25% return on investment. However, our professional advisors have told us not to expect greater than 4.8% over the next ten years. If that projection comes true, our unfunded liability for the County doubles to around $5 Billion and the county’s pension cost projections are also significantly off base.

While I believe the Board missed an opportunity last year to truly address our pension issues and develop an overall compensation plan that would provide a mix of salary, pensions, and benefits that would attract the best employees and teachers, these changes are another important step. I look forward to working on further reforms to the county’s pensions so that we will be able to continue to provide the high-quality services important to you without having to raise taxes.

The foregoing was first published in The Herrity Report, January 17, 2017.

Photo Credit: Pixabay