Governor Abigail Spanberger so far is no more clear on her tax and spending priorities than Candidate Spanberger was, but her fellow Democrats in the General Assembly are laying out a smorgasbord of tax increase options for her.

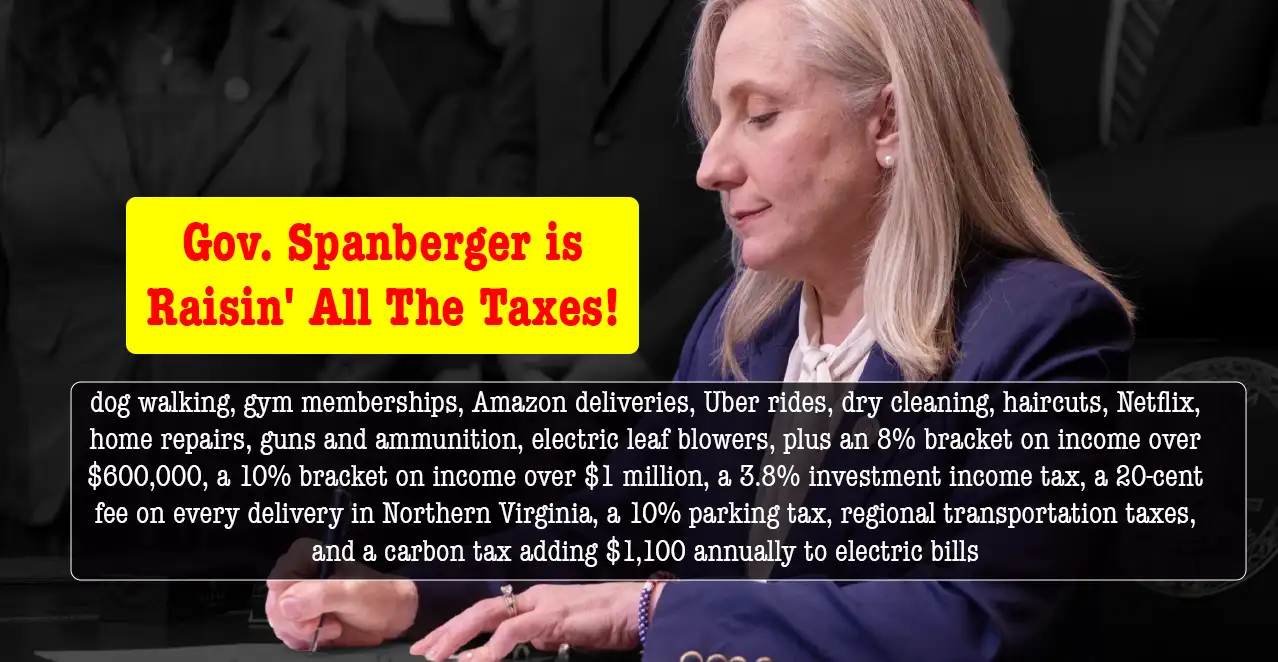

Would she like a major “tax the rich” approach? Start with Delegate Vivian Watt’s House Bill 979, pending in the committee the Fairfax Democrat chairs. It would create two new tax brackets on taxpayers with higher incomes, 8% on taxable incomes higher than $600,000, and then rises to 10% on income of more than $1 million.

Do you want to tax upper income families another way? Many get much of that income from investments, and House Bill 378 from another Northern Virginia Democrat imposes a 3.8% piggyback income tax on net investment income reported on their tax returns. It will not kick in until $500,000 in such income is received. That is the same supplemental tax rate as is applied by the federal Net Investment Income Tax, but HB 378 uses a higher threshold before the tax starts.

For some individuals, the combination of the two bills would impose a state tax rate of 13.8% on part of the investment portion of their reported income. That would move Virginia into the high tax atmosphere shared with a few other states, as one observer noted.

But it impossible to imagine the Assembly Democrats pushing that idea forward for Governor Spanberger’s approval unless the governor asked them to do so, either publicly or privately. The first question she needs to answer is whether she wants a large or even a small amount of additional tax revenue to expand the spending in departed Governor Glenn Youngkin’s $211 billion budget (which was 50% higher than just five years ago).

Traditionally, new Governors do make substantial changes to the departed Governor’s budget, done through a series of budget amendments. There are no Governor’s Amendments pending yet among those already filed at the General Assembly, nor have any presentations of her wishes been made to the money committees. That could happen soon.

How much larger a budget she is looking to approve should drive what level of tax changes, if any, she will support. The process may go forward out of public view, with the first information on just how much more the new Governor wants to spend, and on what is appearing with the House and Senate bills on Sunday, February 22.

Sadly, it has become standard practice to use those bills to also adopt any tax policy changes needed to fund them – raising or lowering taxes. The days when the tax policy was set in advance of the budget are gone.

There are two substantial tax increases Spanberger has clearly endorsed. She wants Virginia back in the Regional Greenhouse Gas Initiative, with its carbon tax of about $550 million it will impose on energy producers and passed on to customers. And she has asked the Assembly to approve a state-managed paid family and medical leave program for workers, funded by a payroll tax of to-be-determined size, divided between employees and their employers. Combined, it will approach 1% of pay.

Governor Youngkin assumed Virginia would conform to several of the provisions of the new federal tax code adopted in July 2025. If the Assembly decides to de-conform instead, and tax things the federal government does not, that will add millions for legislators to spend. That would be the result of Senate Bill 664.

The income tax bills listed above, plus another with a 10% tax on $1 million in income, would generate massive additional revenue. None of the three bills have received those estimates from the Department of Taxation. Raising the income tax is not the only way to fatten the state treasury.

Watts also has a bill to expand the sales and use tax to services, House Bill 978, again still lacking a fiscal impact estimate. The entire services sector would be brought into the sales tax regime, including but not limited to admissions, recreation facilities, repairs, counseling, deliveries, dry cleaning, shipping and travel. Both digital services and digital goods would be covered by the tax, which is now 7% in some localities.

Expanding the sales tax to all those services and digital personal property would be a tax bonanza for both the state and the localities, which share in the sales tax. Many localities have supplemental local sales taxes ostensibly for schools, and that practice will become near universal under House Bill 334 or Senate Bill 607.

Another bill to expand the sales tax to services, House Bill 900, also layers on a higher sales tax rate in the Northern Virginia Transportation Commission’s localities. That bill also imposes in those localities a flat 20 cent “doorstep tax” on deliveries of any non-food items, which has proven controversial in other states.

A large state tax increase results if the General Assembly allows two major income tax rules to expire. Absent legislation, this is the last year for the standard deduction to be $8,750 per person or $17,500 per couple. It would revert to the pre-Youngkin level of $6,000 per couple. An enhanced Earned Income Tax Credit (EITC) could also expire if nothing is done.

Republican legislation to make both permanent has already been defeated in the Senate, but the Senate Finance and Appropriations Committee chairperson has Senate Bill 662 pending to extend them for two years (think past the next election).

Watt’s bill to create the new high income tax brackets includes two provisions that the Thomas Jefferson Institute for Public Policy has always supported. Her bill would increase the standard deduction to $20,000 per couple and would begin to index various portions of the state tax code. Creeping inflation erodes the value of deductions and credit and brings more income under the state’s frozen top tax bracket of $17,000, unchanged for decades.

Are those positive aspects of her proposal sufficient to win the Thomas Jefferson Institute’s support or at least acceptance of the high-income provisions? No.

Very few families would be impacted by the $1 million bracket or the tax on investment income above $500,000 (not Watts’ bill). But those families would be highly motivated to leave Virginia, or to move their income into some tax haven. Virginia should not be raising its income taxes when so many other states, including our immediate neighbors, are lowering them.

Steve Haner is a Senior Fellow for Environment and Energy Policy. Steve Haner can be reached at Steve@thomasjeffersoninst.org.